Featured Resources

ALTA Insights Webinar

ALTA Insights Webinar

TRID Ready? This Is What It Looks Like

Watch this webinar to learn the initial perceptions of the then-new TRID rule. The presenters cover the lender Perspective, Title/Settlement Agent Perspective, Technology, What Your Real Estate Partners Should Know and What Consumers Should Know.

TitleNews Article

TitleNews Article

CFPB Releases Findings From TRID Assessment Report

The Dodd-Frank Wall Street Reform and Consumer Protection Act requires the Consumer Financial Protection Bureau to review some of its rules and issue reports within five years after they take effect. In November 2013, the bureau issued its final TILA-RESPA Integrated Disclosures Rule rule, which went into effect Oct. 3, 2015.

HR Document

HR Document

TRID Preparedness Checklist

Title agents can use this checklist to make sure their IT equipment is ready to handle the TRID upgrade.

Advocacy & Policy

TRID Final Rule for Integrated Mortgage Disclosures

Read the entire rule from the Consumer Financial Protection Bureau (CFPB). The rule is effective August 1, 2015.

Meetings & Education

The Need for Electronic Collaboration: Solutions to Effectively Share Data for TILA-RESPA Integrated Disclosures

Don Partington of Fidelity National Title Group, Ethan Pack of Stewart Title and Steve Acker of Closergeist

5 Key Areas to Prime Your Operation for the New Closing Process

Cynthia Blair NTP, Blair Cato Pickren Casterline Shari Schneider, Stewart Title of California Sheila Strong, AmeriFirst Home Mortgage Leslie Wyatt, SoftPro

New Era In Closings Prepare Now for the CFPB's Integrated Mortgage Disclosures

The August 2015 implementation deadline for the Consumer Financial Protection Bureau's integrated disclosures will be here before we know it.

Resources & Tools

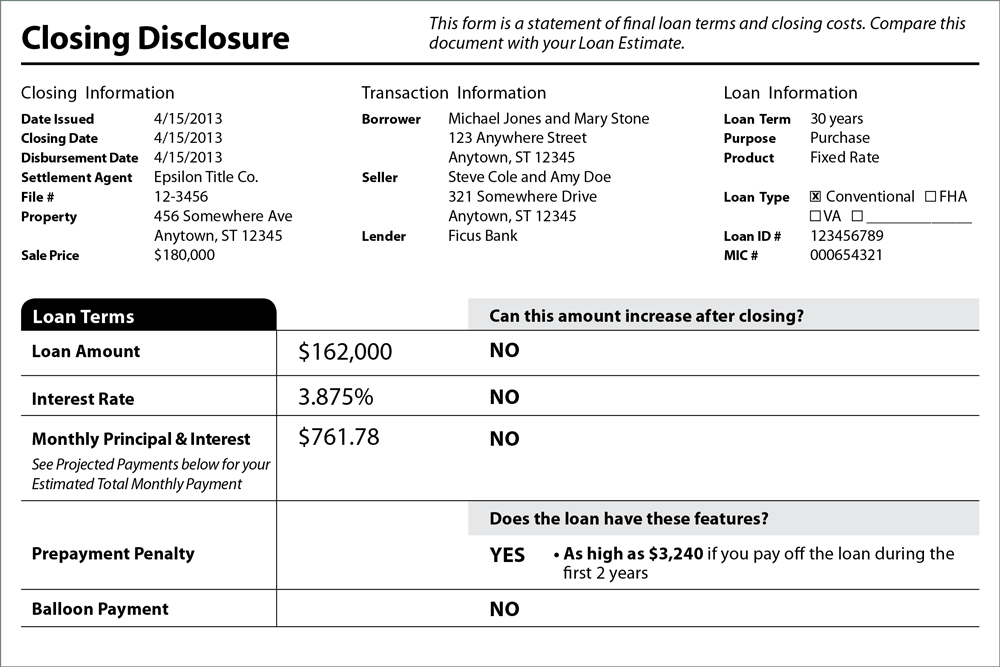

Closing Disclosure Example

Lenders are required to provide your Closing Disclosure three business days before your scheduled closing.

Loan Estimate Example

When a homebuyer receives a Loan Estimate, it should reflect a particular loan discussed with a lender.

News & Insights

ALTA Supports House Passage of Housing for the 21st Century Act

ALTA applauded the U.S. House of Representatives for passing the bipartisan Housing for the 21st Century Act, legislation aimed at modernizing federal housing policy and expanding access to safe, sustainable homeownership. The bill was passed by a vote of 390-9.

ALTA Thanks 2025 TIPAC Donors

The Title Industry Political Action Committee is ALTA's voluntary, non-partisan political action committee (PAC). TIPAC raises money to help elect and re-elect candidates to Congress who understand and support the issues affecting the title industry. In 2025, TIPAC raised $551,890 from 773 people. In addition, 24 companies pledged $150,000 to the TIPAC Education Fund. Read on to learn more about TIPAC.

State Legislation Tracker Map

ALTA provides a state legislative map that allows members to track bills that impact the title and settlement industry in all 50 states and Washington, D.C. The interactive map can be searched by bill number, by state and by topics. Users can click on each bill to get more information. The map and list are updated daily.

Kurt Pfotenhauer Leaves Legacy Championing the Title Insurance Industry

Kurt Pfotenhauer stands as one of the most influential figures in the American title insurance and real estate finance industry. His leadership, advocacy and strategic insight have helped shape how the industry engages with policymakers, lenders and consumers, promoting the vital role of title insurance in the homebuying and refinance process. Pfotenhauer, executive vice president and vice chairman of First American Title Insurance Co., passed away Jan. 21. He served as CEO of ALTA from 2008 to 2011.

ALTA Urges Congress to Recognize Fraud Prevention as a Key Housing Affordability Tool

In a letter submitted for the record to the House Committee on Financial Services, ALTA urged lawmakers to recognize fraud prevention as a critical—but often overlooked—component of housing affordability. The letter was submitted in connection with the committee’s hearing titled “Oversight of the Department of Housing and Urban Development and the Federal Housing Administration.”

White House Issues Executive Order to Limit Institutional Buying of Single-family Homes

President Donald J. Trump issued an executive order Jan. 20 aimed at curbing large institutional investors from buying up single-family homes. The order, titled “Stopping Wall Street from Competing with Main Street Homebuyers,” directs federal agencies to take steps that would prioritize individual owner-occupants over large institutional investors in the acquisition of single-family homes.

How Fraud Impacts Housing Affordability

Housing affordability is about more than home prices and interest rates—it also depends on strong fraud prevention. When real estate fraud goes unchecked, hidden costs ripple through the housing system, driving up expenses for buyers, lenders and communities and making homeownership harder to achieve. Use this handout to help explain how fraud impacts housing affordability.

Five Questions About Values in the Title Industry

A company’s values are the cornerstone of its culture. They are the basis of how a business functions. They set you apart from the competition, make you unique and are essential to achieving an organization’s goals. In this article, we talk with Amy Gregory, chief administrative officer/president of title operations of Florida Agency Network, who shares why ALTA’s Our Values are important for the industry and her company.

TRID Document Center

ALTA has developed standardized ALTA Settlement Statements for title insurance and settlement companies to use to itemize all the fees and charges that both the homebuyer and seller must pay during the settlement process of a housing transaction. Settlement statements are currently used in the marketplace in conjunction with the federal HUD-1. The ALTA Settlement Statement is not meant to replace the Consumer Financial Protection Bureau's Closing Disclosure, which went into effect on Oct. 3, 2015. Four versions of the ALTA Settlement Statement are available.

This information is not a substitute for legal advice, is for your reference only, and is not intended to represent the only approach to any particular issue. This information should not be construed as legal, financial or business advice, and users should consult legal counsel and subject-matter experts to be sure that the policies adopted and implemented meet the requirements unique to your company.